(Image credit: Getty Images)

When it comes to building wealth, most people obsess over picking the right stocks or timing the market. But the real secret isn’t really a secret. It’s just time.

Compound interest works like a quiet engine, steadily multiplying your money in the background.

And the earlier you start, the more powerful that engine becomes.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

Think of it as money’s superpower: Small contributions today can snowball into life-changing sums decades down the road.

That’s why time isn’t just an investor’s friend; it’s their greatest asset.

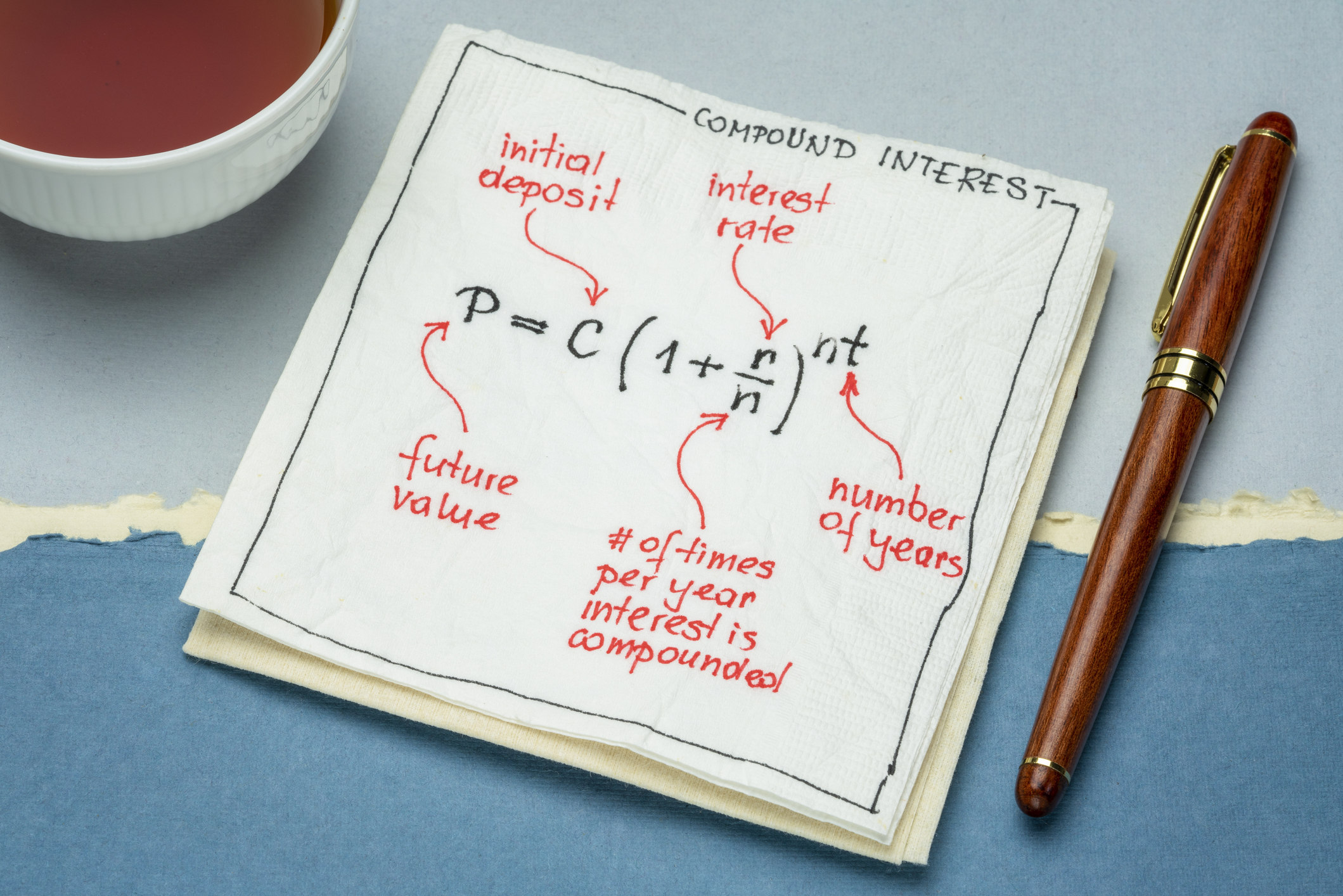

What is compound interest?

Compound interest is the process of earning interest on your interest.

It may sound confusing, but “anyone who has ever made a snowman is familiar with the concept of compounding,” says Wes Crill, senior client solutions director and vice president at Dimensional Fund Advisors. “What starts as a small ball of snow grows as it’s rolled further. Each time it grows, there’s more surface area to which snow can stick.” As a result, the girth of the ball grows exponentially, “until you end up with an Olaf replica.”

A similar process happens with your money where each additional earning effectively picks up more earnings.

For example, if you invest $1,000 and generate 10% compound interest, you’ll make $100 in the first year. This gives you $1,100 to earn interest on in the second year. So, you earn $110 in interest that year.

It may seem small at first, but compound interest can rapidly add up.

Forty years after your initial $1,000 investment, assuming you continue earning 10% per year and don’t take any funds out, you would have earned $44,259.26 in interest, all from that single $1,000 investment.

This is different from simple interest, which only calculates earnings based on the original amount you invested.

With simple interest, you’d only earn $100 per year, unless you added more funds. S0, 40 years later, you’d have made only $4,000 in interest.

This is why Albert Einstein is rumored to have called compound interest the “eighth wonder of the world.”

(Image credit: Getty Images)

How to make the most of compound interest

To transform the passive concept of compounding into an active wealth strategy, you need to commit to three strategic habits.

Start young

Compound interest is only as powerful as the time you give it to work its magic. Like popcorn kernels, if you aren’t patient, you’re left with a handful instead of a full bowl.

The earlier you start, the better. And you can do it automatically.

“It’s better to invest even a little bit every month when you are young, because that little bit can become a lot over the years, and especially over the decades,” says Andrew Crowell, financial adviser and vice chairman of Wealth Management at D.A. Davidson.

Take the above example: If you only gave that $1,000 investment 15 years to grow, it would only have earned $3,177.25 in interest at a 10% annual return.

Even if you contributed an extra $1,000 per year for all 15 years – so your total contributions became $15,000 instead of $1,000 – you’d end up with less money in the end ($39,126.98 instead of $45,259.26).

Consistency over timing

Successful compounding requires a continuous commitment, not perfect market timing. For compounding to work, your money needs to stay invested through thick and thin.

Trying to time the market can sabotage your long-term wealth by robbing you of valuable time in the market.

“Missing only a brief period of strong market performance can drastically affect your lifetime wealth,” Crill says. He gives the example of $1,000 invested in 2020. Left in a Russell 3000 index fund until 2024, it would have grown to $6,064.

But if you missed just the single best week during the time period, it’d only be worth $5,511. If you missed the three best months, you’d be left with nearly $2,000 less.

“Thinking about investments in a long-term framework might dull the temptation to make asset allocation changes that studies have shown are a recipe for disappointment,” he says. “And over the long term, the market has been a powerful ally in building wealth.”

Reinvest every penny

One of the easiest ways to maximize the power of compounding is to reinvest your dividends, interest and capital gains. In fact, failing to do this would derail you entirely because for compounding to work, your earnings need to be available to make more earnings.

This isn’t an active choice you should have to make every quarter; it should be an automated setting in your investment accounts.

By selecting the option to reinvest dividends and capital gains, you ensure that the growth is always compounding on a larger and larger sum, year after year.

You can also aim to increase your contributions for a turbo boost. Matthew Mandell, a private wealth adviser at Ameriprise Financial, advises clients to increase savings gradually so money doesn’t get spent elsewhere.

“Consistency and patience are key,” he says.

(Image credit: Getty Images)

The biggest threats to long-term growth

The compounding engine is durable, but several common missteps can throw a wrench in the works, sabotaging years of patient growth.

Lack of diversification

Diversification is one of the most common terms bandied about in the finance industry for good reason.

True wealth is built on a broad, well-diversified base. Compounding requires a level of security.

If you focus all your capital on one high-growth company or a single risky asset, a catastrophic event can wipe out your entire principal.

By spreading your capital across different asset classes, sectors and geographies, you ensure that even if one segment struggles, the rest of your portfolio continues to generate the returns you need to fuel your compound growth.

Yielding to market panic

The stock market is a volatile place, and corrections are a normal part of its cycle. Selling during a dip locks in the loss and, more importantly, takes that capital out of the market entirely, stopping the compounding process dead in its tracks.

It also makes recovery harder. “Large withdrawals, especially after a downturn, can shrink your ‘snowball,'” Mandell says. “For example, a 50% loss requires a 100% gain just to break even.”

For a compound investor, a market downturn is simply a temporary opportunity to buy more quality assets at a discount.

“Over time we know that markets rise more than they fall, so it’s important for a saver to be diversified and ride out the downturns,” Crowell says.

Frequent trading and “The Drag”

Compounding rewards stability. Short-term, active trading is like trying to build your snowman under a heat lamp.

When you frequently buy and sell, you introduce significant drag on your portfolio’s growth. This drag comes from transaction costs and tax inefficiency, both of which can erode your principal, even at small amounts.

If you want to maximize your long-term growth, focus on “tax-deferred or tax-free accounts, and avoid high-cost funds and unnecessary short-term trading,” Mandell says.

Finally, a note of caution: “Compounding works in both directions, so keep your debt in check and pay off those credit cards each month,” Mandell says.