Artificial intelligence (AI) stocks have lost their luster in recent months, which seems surprising given that companies in this sector have been reporting strong growth quarter after quarter.

The poor performance of AI stocks explains why the tech-focused Nasdaq Composite index has slipped 11% over the past three months. The war in the Middle East, the rising probability of a recession, and higher fuel prices have dented investor confidence in the stock market this year, and AI stocks have borne the brunt.

However, it will be worth looking past the noise. AI companies continue to grow at a terrific pace, driven by heavy infrastructure investments in data centers and by customer adoption of this technology. Also, their valuations are now relatively cheaper due to the sell-off. With AI expected to contribute a whopping $22.3 trillion to the global economy by 2030, according to IDC, I would treat the recent pullback in AI stocks as a buying opportunity.

Here are some of the top names in this sector I’d consider buying before the market starts rewarding their solid growth.

Image source: Getty Images.

These software companies are helping customers reap the benefits of AI

Shares of Snowflake (SNOW +1.52%) and Palantir Technologies (PLTR +0.14%) have slipped 32% and 24%, respectively, over the past three months. However, both companies are benefiting from the rapid adoption of their AI software solutions.

Today’s Change

(1.52%) $2.30

Current Price

$153.12

Key Data Points

Market Cap

$52B

Day’s Range

$148.20 – $155.44

52wk Range

$120.10 – $280.67

Volume

5.1M

Avg Vol

6M

Gross Margin

66.12%

Snowflake, a cloud-based data platform provider that traditionally provided data storage and analytics solutions, has been offering multiple AI solutions to help customers get more out of their data. It has been infusing AI in its data cloud platform for the past three years, enabling customers to build and deploy AI applications using their proprietary data. Also, Snowflake’s AI agents help improve customers’ decision-making by analyzing their data and offering suggestions.

Not surprisingly, the company has been witnessing a solid surge in the adoption of its AI products. CEO Sridhar Ramaswamy noted on the February earnings call:

Key to our growth is the strength and momentum around our AI products. This quarter, we delivered the largest sequential increase in accounts using AI, bringing the total to more than 9,100 accounts. And in just three months, Snowflake Intelligence has scaled from a nascent offering to an essential capability for over 2,500 accounts, almost doubling quarter over quarter.

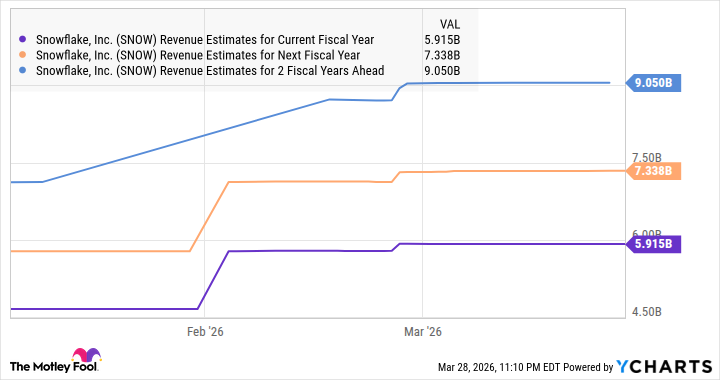

The improving adoption of AI is translating into healthy growth for Snowflake. It ended fiscal 2026 (which ended on Jan. 31, 2026) with a 29% increase in product revenue to $4.47 billion. Even better, the company’s remaining performance obligations (RPO), which is the total value of contracts yet to be fulfilled at the end of the quarter, increased by a much stronger pace of 42% to $9.77 billion.

This puts Snowflake in a position to exceed its fiscal 2027 product revenue guidance of $5.66 billion, an increase of 27% from the prior year. Even analysts are expecting Snowflake’s growth to remain robust:

SNOW Revenue Estimates for Current Fiscal Year data by YCharts

With the stock trading at 12 times sales right now, it would be a good time to buy Snowflake before it regains its mojo.

Meanwhile, Palantir’s expensive valuation continues to weigh on the stock. It trades at 116 times forward earnings and 86 times sales despite the recent pullback. However, Palantir doesn’t seem expensive when you consider its growth and prospects.

The AI software platforms market in which Palantir operates is poised to grow at an annual rate of 40% through 2030, according to market research provider Technavio. The company adds that there is a $100 billion incremental revenue opportunity in this space over the next five years.

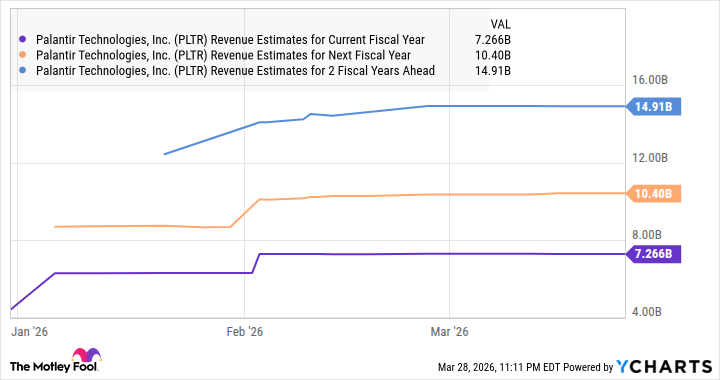

Palantir is one of the best ways to capitalize on this market. The solid improvements in the company’s customer base and its ability to expand existing customer contracts have led to strong revenue and earnings growth. The company’s revenue jumped by 70% in Q4 2025 to $1.4 billion, along with a 79% year-over-year increase in adjusted earnings to $0.25 per share.

But what’s worth noting is that Palantir signed a record $4.3 billion in new contracts during the quarter, up 138% from the prior year. The fact that Palantir’s contract value grew at 3 times the pace of its revenue last quarter suggests it can sustain its terrific growth momentum. Not surprisingly, analysts are expecting its top line to double in just two years (using the 2026 revenue estimate as the base).

PLTR Revenue Estimates for Current Fiscal Year data by YCharts

Palantir stock can justify its valuation and start soaring once again as it converts its sizable backlog into revenue. That’s why growth-oriented investors will do well to buy the dip.

This underrated hardware play is showing signs of rebounding

Marvell Technology (MRVL +7.70%) may not be as well known as other AI chip designers, but it is gradually becoming an important player in this market. The stock shot up remarkably in March after the company reported better-than-expected results and impressive guidance.

Today’s Change

(7.70%) $7.63

Current Price

$106.68

Key Data Points

Market Cap

$93B

Day’s Range

$100.50 – $107.84

52wk Range

$47.09 – $107.84

Volume

1.9M

Avg Vol

18M

Gross Margin

50.10%

Dividend Yield

0.22%

Marvell designs custom AI processors that are in high demand from hyperscalers. Bloomberg estimates that shipments of custom AI processors could increase at a 21% compound annual rate through 2033. Marvell is well positioned to capitalize on this opportunity, as it designs custom processors for Amazon and Microsoft, according to Bloomberg.

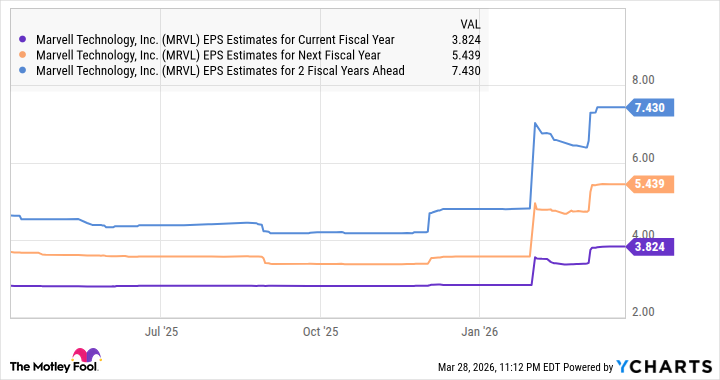

However, Marvell’s AI customer base is expanding rapidly, with the company bringing in more hyperscalers into its fold. This is translating into terrific earnings growth for Marvell. Its bottom line jumped nearly 81% in fiscal 2026 (which ended on Jan. 31, 2026) to $2.84 per share. The healthy prospects of the custom AI processor market indicate why its bottom-line growth is set to take off.

MRVL EPS Estimates for Current Fiscal Year data by YCharts

Marvell’s impressive earnings growth can send the stock soaring, which is why it is worth buying the stock hand over fist as it is trading at just 23 times forward earnings right now.