Micron Technology (MU 10.13%) is a candidate for stock of the year halfway through 2026. Its shares are trading up about 309% so far in 2026, making it the second-best performing stock in the S&P 500 (^GSPC 0.22%), trailing only Sandisk, another memory chipmaker. Its newfound success has also allowed it to join the $1 trillion valuation club.

But after the stock has quadrupled to start the year, there are obvious questions about how much upside is left. Let’s take a look at Micron’s business to see if its stock is one to buy now or one to avoid.

Image source: Getty Images.

Memory chip demand isn’t slowing down

Micron is caught in the middle of the biggest demand wave memory chip companies have ever seen. The data center build-out has required an immense amount of memory, and companies like Micron do not have nearly the capacity to meet demand. When there is a huge demand and low supply, prices skyrocket, and that’s exactly what’s driving Micron’s stock price higher.

This increased demand isn’t expected to resolve anytime soon, as Micron believes the memory chip supply crunch will persist beyond calendar year 2027. That means these elevated prices are here to stay, and even with Micron opening new production facilities in 2027, it still may not be enough to drive prices down.

Today’s Change

(-10.13%) $-116.88

Current Price

$1037.41

Key Data Points

Market Cap

$1.2T

Day’s Range

$1036.28 – $1096.86

52wk Range

$103.38 – $1255.00

Volume

13.5K

Avg Vol

51.2M

Gross Margin

72.60%

Dividend Yield

0.05%

That creates a bullish environment for Micron’s stock, and its finances back it up. During Q3 of fiscal year 2026 (ending May 28), Micron’s revenue rose a jaw-dropping 346% year over year to $41.5 billion. For reference, Micron provided guidance for $33.5 billion. That’s a huge guidance beat, but it’s far from done. Next quarter, Micron expects $50 billion in revenue. Growth is clearly driving Micron’s stock, and it’s the major reason the stock was up so much following the announcement, but is there still room to run?

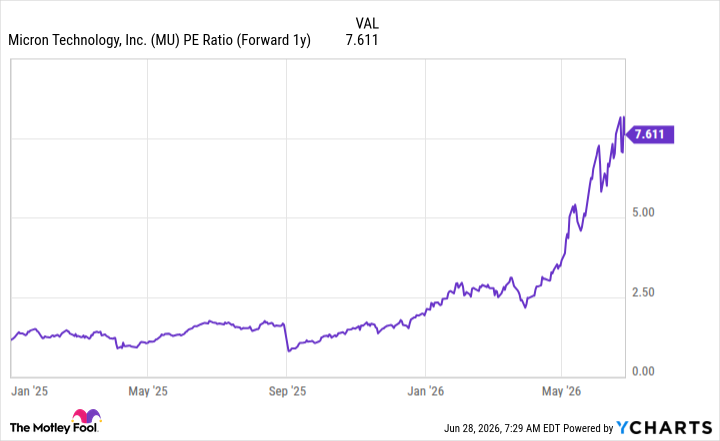

Since the quarter underway is Micron’s Q4, I think it’s best to start valuing the stock on fiscal year (FY) 2027 earnings, which would start in September. From that perspective, Micron’s stock trades for a cheap 7.6 times forward earnings.

Data by YCharts.

The S&P 500 trades for 21.5 times forward earnings, and many big tech stocks can trade for far higher. That suggests Micron’s stock could still have a long way to run, especially if the memory chip crunch persists beyond 2027.

As a result, I think investors can purchase Micron’s stock now and still have solid gains over the next few years.